The Illusionary Moat: BiliBili

The Illusionary Moat: BiliBili

A 15-Minute Pitch

Introduction

This article is both an investment thesis for BiliBili and a demonstration on how I think about investing in general — which would change throught my life (I’m 21), and career.

After being down c.85% from peak, and frequently seeing them on various headlines, I was curious to know what happened, and figured that it would also be a great start to learn about Chinese equities. After spending some time researching and learning about their business, I think that the are missing pieces of crucial information around the stock and current narrative serves to sugarcoat their non-existent moat. With that, I’m proposing a short on BiliBili with a 1-year PT of 118HKD / Share, down c.24.5% from its current levels.

An Overview of BiliBili

BiliBili is China’s popular video streaming website with a strong ecosystem of user generated content (c.94% of total content). They started as a community-driven platform where ACG (Anime, Comic, and Games) fans would stream, share, and talk about anything ACG-related, sometimes becoming a safe haven for people to confide in.

However, several angel investments, and VC fundings later, BiliBili found themselves at a crossroad — culture or monetization, to which they chose the latter. This started in 2015 when they expanded to mobile gaming, and employed a subscription model for their services afterwards. This was poorly received by the platform’s early adopters but was effective in attracting new users, leading to a c.40% CAGR in MAU from ’15 to ‘22.

BiliBili did their public listing at the New York Stock Exchange on March 2018, raising US$443mn in net proceeds. This attracted strategic partnerships from big technology companies such as — 1) Tencent acquiring c.13% of BiliBili on October 2018 to operate and share their existing anime & games on BiliBili’s platform, and 2) Alibaba acquiring c.7% of BiliBili on December 2018 to expand their content-driven e-commerce and help BiliBili commercialize their IP. This can also be perceived as a way for Tencent / Alibaba to keep BiliBili under control.

Then, BiliBili did a dual listing in the Hong Kong Exchange on March 2021, raising US$2.92mn.

The timeline of BiliBili’s progression can be seen as follows:

Business Model / Revenue Streams

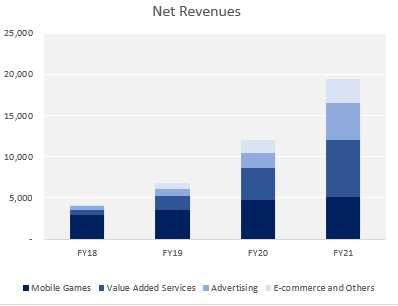

BiliBili now operates a diversified revenue model based on their initial video-sharing ACG platform with bulk of their CY21 revenues coming from their legacy offerings — 1) Live-streaming (c.36% of CY21 revenue), and 2) Mobile gaming (c.26% of CY21 revenue).

Their live-streaming revenue falls under Value-Added Service (“VAS”) and is a blend between — 1) Subscription fees of premium membership program, and 2) Sale of virtual items for use during the livestream, and 3) Paid content.

On the other hand, their gaming segment operates a non-recurring model for both exclusive (i.e., Local rebranding, c.71.3% of mobile game revenues in CY21) and JV games (c.28.3% of mobile game revenues in CY21)— almost all revenue in this segment is derived from virtual in-game item sales to which the net ratio is determined on a contractual basis with the 3P game developers when performance obligations are satisfied (i.e., Sales threshold).

However, Advertising, and e-commerce (i.e., Sale of ACG related products) which comprises of the remaining c.23%/c.15% of their revenues are currently the highest growth segment. BiliBili’s full-suite product offering can be seen below:

Summary of Investment Thesis

BiliBili has taken quite a hit due to the regulatory headwinds faced by Chinese gaming and online entertainment companies, drawing their stock price down c.85%+ from their peak in July 2021. This has led to the market calling bottom for the stock, and attributing their impressive user growth to a potential upside. However, I believe that there is more to BiliBili’s story that is overlooked, and will be discussing them as a 4-part investment thesis below:

Regulatory crackdown in China is just starting

Unscalable unit economics stemming from a poor quality user base

Significant competitive pressure from tech giants

Questionable management team

BiliBili’s growth story began in 2015 when they earned licensing right of an ACG game named Fate Grand Order from Sony which caused net revenues to implode upwards at a c.70%+ CAGR.

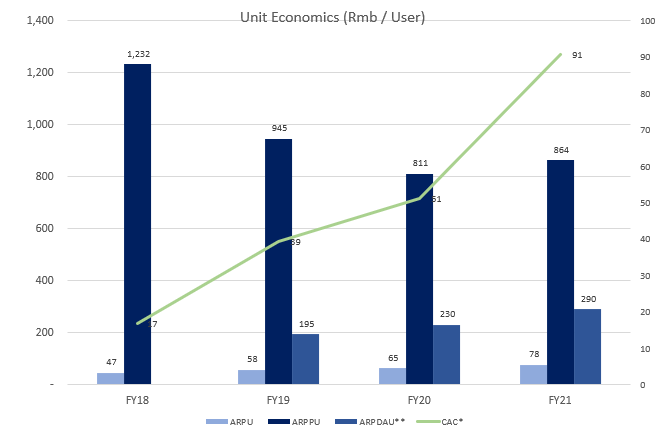

However, despite significant top-line growth, BilIBili faces deteriorating unit economics with customer acquisition costs increasing 5-fold, and average revenue per paying user (ARPPU) decreasing to only 1/2th of where it was 3 years ago.

I believe these poor economics will catch up and stagnate their growth within the next fiscal year, driven by the following factors:

Extension of COVID lockdowns and logistic bottlenecks

New policies limiting advertisement budget

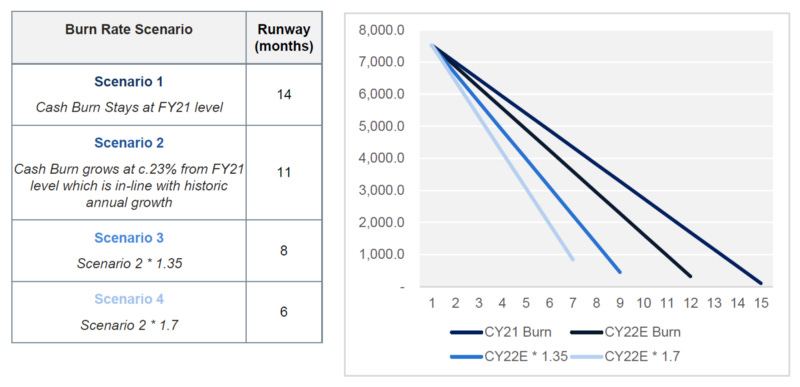

Balance sheet will not be able to keep up with cash burn (i.e., 7–15 month at max — See below)

Regulatory Crackdown in China — and why I think it is just starting

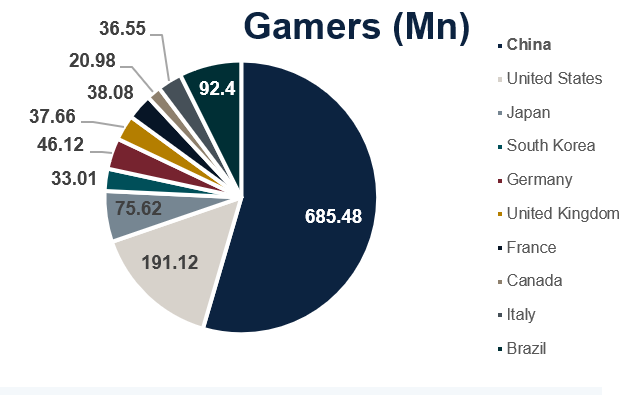

The main premise of the regulatory crackdown stems from an increasing concern over gaming addiction in China as they host the highest population of gamers worldwide with c.685mn gamers, as opposed to the US which is their far second, hosting 1/3 less gamers despite having higher revenue per gamer (i.e., ~4x of Chinese gamer).

Not only do they have the highest gaming population, they also boast the most addicted gamer base of all, with c.52% of their gamers playing more than 6 hours per week — significantly higher than the US (c.44%), and UK (c.38%) who are 2nd and 3rd in gaming addiction.

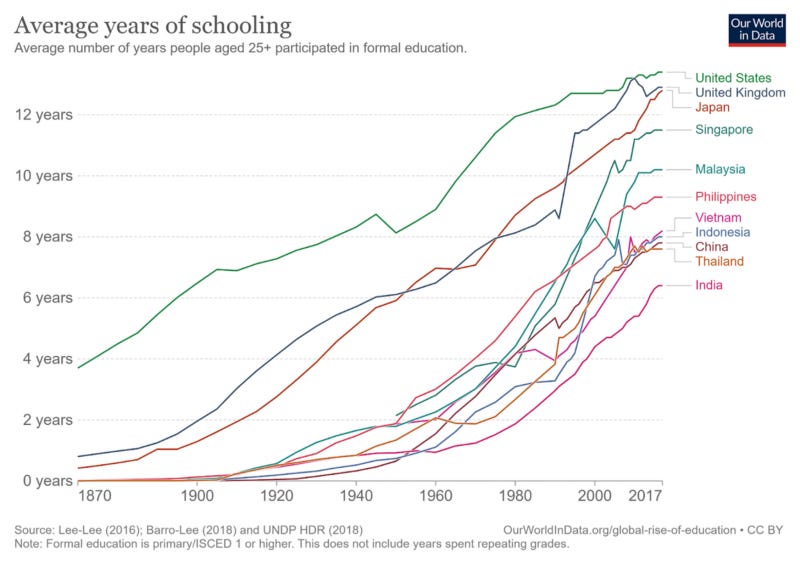

A study done by comunicarjournal in 2020 showed an inverse correlation between number of hours played and academic performance. The results helps in explaining the ~3+ years gap of mean schooling years between China and other developed countries (i.e., US, UK, JP, and SG), highlighting the compromise on educational attainment as a consequence of high gaming addiction.

Their levels as of 2019 is on-par / slightly lower to emerging market countries such as Indonesia, Vietnam, and Thailand at around ~8 years of mean schooling years (see below).

Another concerning factor related to gaming is Myopia (i.e., Nearsightedness) as a study published by british journal of ophtalmology states that children who spend more than 3 hours / day in front of a digital device are 4x more likely to become myopic.

Therefore, with East Asia (i.e., China, and others) boasting a ~10% higher myopia prevalence than global average provides an added rationale for the high crackdown and control on online gaming, especially for minors.

On the other hand, China has also been imposing stricter control on online content circulation, banning everything that contains even a slight element of violence / pornography / terrorism / gambling / superstition which are quite heavily portrayed in successful ACG titles. For instance, the popular video game ‘Grand Theft Auto (GTA)’ is a gangster-themed title where players are free to hijack, and murder people in the game.

This had a huge material impact to BiliBili as they were forced to retract various titles which were quite popular within the ACG/Gaming community among which were Grand Theft Auto and Mushoku Tensei (i.e., Highly rated series on My Anime List).

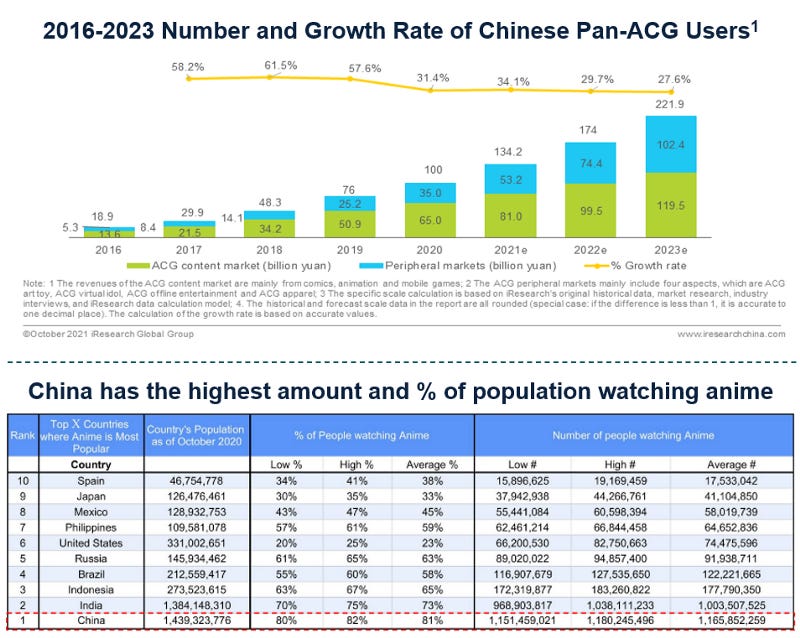

This imposition not only materially affects the Chinese online entertainment industry but also ripples throughout the worldwide ACG community given that the industry was a major contributor to global growth (i.e., Has been growing upwards at a c.25% CAGR p.a since ‘2016 to a US$66bn industry), and a major source of demand (i.e., China has the highest number and % of people watching anime as seen below).

Here are some of the regulations that have been impacting BiliBili:

Transmission of Audio-Visual Content — Prohibits content containing violence, pornography, gambling, terrorism, or other prohibited elements.

Anti addiction system for minors — Minors are required to register game with valid identity information, with play time limited to no games between 10pm — 8 am the next day on weekday and only 1 houre between 8–9 pm on weekend & public holidays. Gme developers should also alter content that may cause addiction.

Online Live Broadcasting Services — 1) 1:50 ratio of content reviewer to broadcasting rooms, 2) Minors are not allowed to virtually gift / manage fan group of idols, 3) Minors are not allowed to create publisher’s account without parent’s consent, 4) Limiting PK to 2 per user during 8:00 pm to 10:00 pm, and 5) Limiting virtual gifting each user may give.

Virtual Currency & Virtual Items — 1) No Virtual Items / Currencies through lottery-based activities, and 2) Limits on amount of virtual currency issued by online game operators and amount purchased.

I would like to highlight the 3rd and 4th as the first is given, and the second is not as material given that c.80% of Bili’s revenue comes from those aged 37+ or older.

As close to ~100% of BiliBili’s gaming revenue is derived from sale of virtual in-game items, limiting the number, and sale of virtual in-game items will materially impact their gaming segment. To add insult to injury, the ban of virtual items through lottery-based activities means that Gacha, a lottery-based in-game mechanism which is a very popular feature of games will hurt not only sales but attractiveness of these games, inducing more churn, deteriorating economics → Same goes for Live Streaming’s attractiveness though they might be more robust given their revenues are derived from a blend of subscription, and sale of virtual in-game item albeit increasing regulations will definitely introduce more churn, and less sales in both aspect.

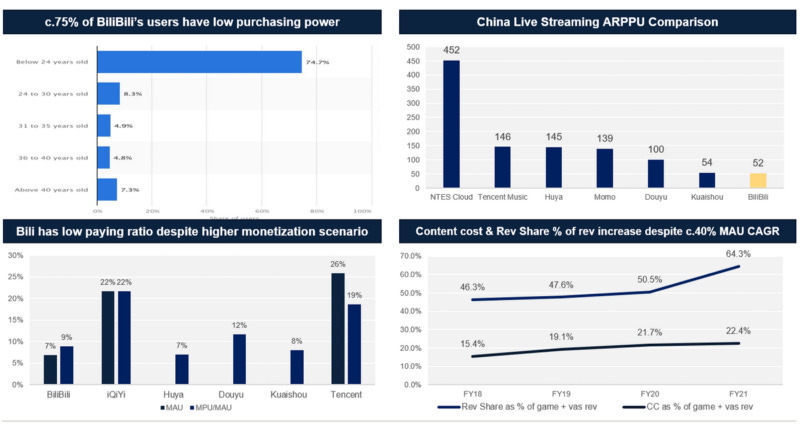

BiliBili has an unscalable unit economics — The user base problem

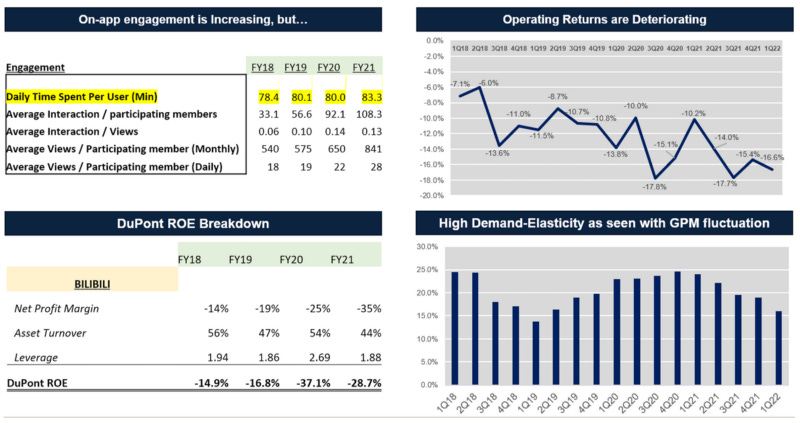

After doing some deep dive into the 3 forces acting on a networked product / business reaching escape velocity (i.e., Engagement, acquisition, and monetization / economics), it was found that 1) Customer Acquisition Cost quintupled in the last 3 year, and 2) Operating returns (i.e., EBIT / Average Asset) deteriorated over time despite increasing engagement, especially time spent per user in-app as seen in the figure below. This suggests the absence of organic viral loops, and pointe towards an unsustainable, inorganic growth.

Furthermore, as seen in the figure above, a c.10% top-line margin fluctuation within a single fiscal year highlighted the lack of the existence of a pricing power / economic moat, typical of a non-ideal business.

The structural mis-match between the engagement, acquistion, and monetization forces can be explained by further looking into their user base which is illustrated in the figure below.

First off, c.75% of their users are aged 24 or younger, and c.50% of them are mainly university students with low purchasing power. In fact, c.80% of their revenue comes from only c.10% of their user base. This explains why BiliBili’s average revenue per paying user is the lowest compared to peers despite having more monetization source than the advertisement-heavy Kuaishou and Douyu.

To their defense, Bili’s management has stated that they have yet to unlock full ad monetization potential as they are still focusing on top-line growth. While it makes sense, I believe that the reason why they are not able to right now is due to the significant churn they will face if they decide to do so given that despite pirated ACG websites are offering 0 fee at the expense of a high advertisement rate to users, c89% of users will / have watched anime on a pirated website, strengthening the ‘cash-poor, time-rich’ user base thesis for BiliBili.

BiliBili has also attributed its lower paying ratio compared to guys like iQiYi and Tencent Videos despite having similar monetization sources to their huge blend of PUGV content. However, at the economics level, BiliBili has failed to give a positive explaination as to why their costs has fallen at a higher % of revenue. These observations drove me to the conclude with high conviction that they can’t monetize the bulk of their user base and risk higher churn rates of these ACG-loving youths if they were to ramp up monetization which is also catastrophic for their investor sentiment given the high fund manager shareholder base (c.83%) who are highly concerned about the growth.

The Competitive Pressure

Noticing that their user base is unmonetizable, BiliBili started to pivot away from ACG content, despite claiming the youth user base to be their competitive moat. This resulted in 2 significant changes for the company:

Decoupling their tightly knit hardcore ACG user base — This was poorly embraced by the ACG-native users as these users are sensitive to commercialization, effectively losing their illusionary top-line user growth at a point.

Risk having to face direct competition from technology giants who dominate the broader entertainment media value chain — For instance, Tencent alone accounts for almost half of the mobile gaming market share, and Tencent’s Kuaishou / Alibaba’s Youku Tudou dominating the video streaming space.

Furthermore, as Alibaba and Tencent are major BiliBili shareholders, holding a c.7.2% / c.13.3% stake respectively in the company, a direct competition will be very disadvantageous to BiliBili given that they are in the chokehold between the two giants.

Tencent / BiliBili — getting sour?

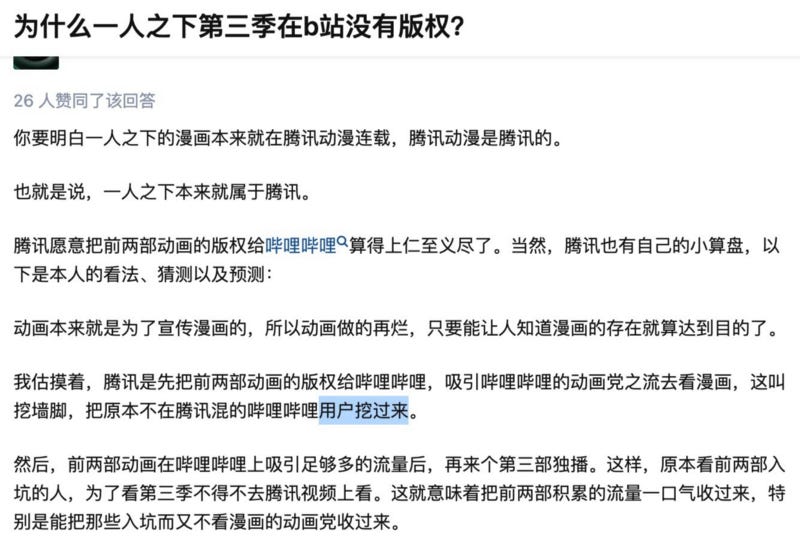

BiliBili entered an agreement with Tencent back in 2018 to share and operate Tencent’s existing ACG and gaming titles in their platform. However, what Tencent was actually doing was to use BiliBili as an initial low-cost touchpoint to tap into their Gen Z+ user base and up-sell them by redirecting to Tencent’s platform.

This was seen with Tencent licensing season 1 & season 2 of a show called One man and Fox Demon while operating season 3 exclusively on their own platform as seen below.

Furthermore, as BiliBili has tried not to offend these technology giants (i.e., Alibaba and Tencent) as it grows, the relationship was cited to have turned sour as BiliBili slowly expanded to all levels of the entertainment industry value chain (i.e., eSports and traditional media shows).

An anonymous Tencent employee interviewed by the Chinese media outlet also stated that BiliBili is now seen “not as a useful partner, but a disobidient opponent”, especially when it comes to livestreaming.

What will happen?

From this, I can think of 2 scenarios — 1) Tencent seeing BiliBili as a good strategic asset for an M&A which is a risk to our short, or 2) Tencent views them as a competitor and decides to shut them down. As of this point, I think the latter is more probable given the unfavourable economics exhibited by BiliBili, and I don’t think there are huge potential upsell for the rest of BiliBili’s unprofitable user base, and this means big trouble for BiliBili.

As a brief visualization of market dyanmics, the following figure shows the market share distribution for mobile gaming and live streaming, 2 of BiliBili’s core legacy segment:

There is no way BiliBili can win especially with the moat these giants possess. For instance, Tencent can just cut off access from BiliBili (i.e., Similar to how Alibaba cuts off Mogu in 2013), and deliberately market their newer titles through their ~1.2bn initial touch point which is WeChat which is a surefire way to gain initial traction irrespective of the quality of the game.

On the other hand, BiliBili mgiht have to burn significant amount of their rapidly thinning balance sheet just to reach a fraction of it. Furthermore, Tencent and Alibaba operates a closed system in China which means that their products are integrated in almost every other element of consumer life, reinforcing their network effects, and acts as a high barrier / deterent to future competition.

Internal Troubles at BiliBili

This section is just to highlight several findings on management, which further strengthens our core thesis but by no means qualified to be a driver for the short.

Despite boasting high insider ownership (c.21.7%), with CEO Rui Chen owning c.12.7%, and Ex-CEO / Founder Yi Xu owning c.7%, BiliBili has failed the testament of a great management / leadership which is the ability to retain key personnel while maintaining a positive working environment. Here are some of their management lowlights:

Glassdoor ratings are trending down in recent years, reaching 3.8 which indicates poor employee satisfaction. Some reviews cite that BiliBili is still operating their business within regulatory grey areas.

Employee turnover rate increased in 2021, with c.27% higher for males, and c.24% higher for females, and the bulk of them being Gen Z+

BiliBili was sued for a copyright issue with South Korean MBC TV in September 2021

In February 2022, BiliBili’s 25-year-old employee who monitored content at BiliBili passed away, allegedly after working from 9 am to 9 pm through the national holiday, citing overwork.

In May 2022, There was a leaked audio recording of management setting impossible mission to force employees to leave, and will fire them if they do not listen.

Catalyst for the short — Regulatory outlook and Strict COVID Policy

Within the short term, I believe that there are 2 major factors that will drive a further deterioration in BiliBili’s stock price, supported by a long term continued regulatory tigthening. The short-term factors are:

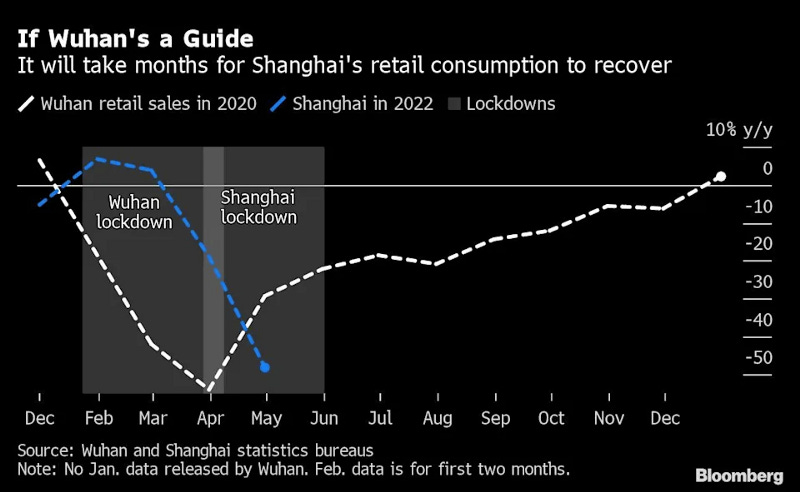

1) Extension of COVID lockdowns and logistic bottlenecks — Lockdown in Shanghai has led to congestion within its Yangtze river ports and shortage of truck drivers as they become more reluctant due to strict zero-covid policy, implying possibility of further lockdowns, halting BiliBili’s e-commerce revenues. Furthermore, as Shanghai supplies c.50% of domestic auto, and is the largest port of entry for cosmetics, advertisement revenue will be impacted given Auto and Cosmetics are key pillars for the advertisement industry 3C and F&B.

If we take the Wuhan lockdown as a benchmark, I believe that advertisement as well as e-commerce spending will not experience significant growth for the next 12 months at the very least as retail consumption wil ltake time to recover.

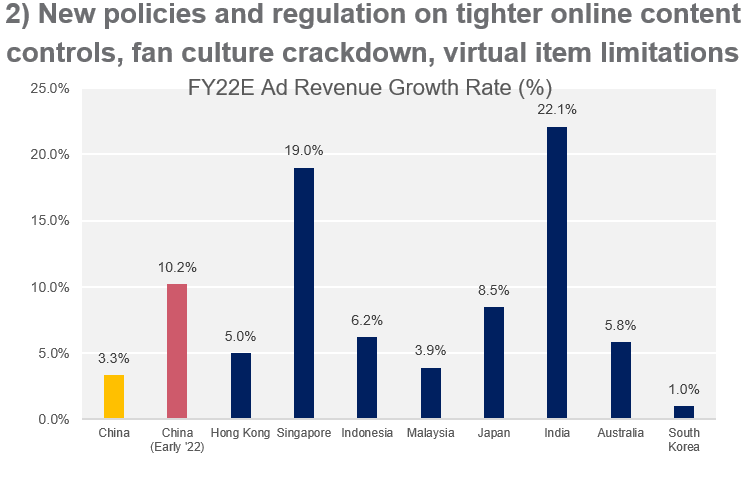

2) New policies further limiting advertising budget — China is only projected to grow by c.3.3% in ad spend YoY vs c.10.2% in GroupM’s previous forecast due to lockdowns in the first half, and policies restricting activities in real estate, education, and the state’s attempt to curtail celebrity-focused “fan” culture within digital platforms will limit growth in general. This will further limit BiliBili’s potential advertising spend, slowing down growth of their highest-margin business.

These short-term catalyst complements the mandate around China’s regulatory mandate around online entertainment to meet their educational and social goals which — 1) Limits BiliBili’s monetization model, and 2) Increases licensing costs as eligible, and highly attractive content becomes increasingly scarce.

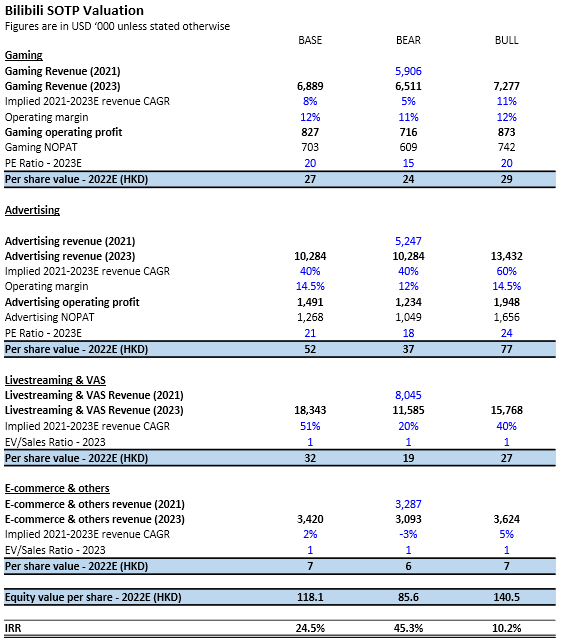

Valuation — SOTP + CC

I used a SOTP valuation for BiliBili’s different business, segmenting them to EBITDA positive business (i.e., Advertising and Mobile Games) and EBITDA negative business (i.e., Livestreaming, and Ecommerce) and applying P/E and EV/sales ratios respectively, giving me a valuation of around 85.6 HKD — 140.5 HKD per share for BiliBili depending on the scenario (i.e., Base / Bear / Bull), representing a c.10% — 45% IRR with BiliBili at 156.5 HKD. The growth rate assumption for base case is as follows:

Gaming Business — Limited growth due to competition and regulation, stunting top-line growth to c.8% CAGR base case. They were growing at c.20% CAGR from ’18 — ’21. Furthermore, I implemented a lower operating margin at c.12% for base case due to higher content costs / licensing fee.

Live Streaming Business — Limited growth due to competition and regulation, stunting top-line growth to c.50% CAGR base case. They were growing at c.128% CAGR from ’18 — ‘21.

Advertising Business — Regulations and supply chain disruption cutting national advertising budget by c.70% puts BiliBili’s advertising business to grow at only c.40% CAGR for base case. They were growing at a c.114% CAGR from ’18 — ‘21.

E-commerce Business — Long consumption recovery and potential future lockdowns further straining supply chain is projected to depress E-commerce growth to only c.2% CAGR for base case despite growing at c.170% CAGR from ’18 — ‘21.

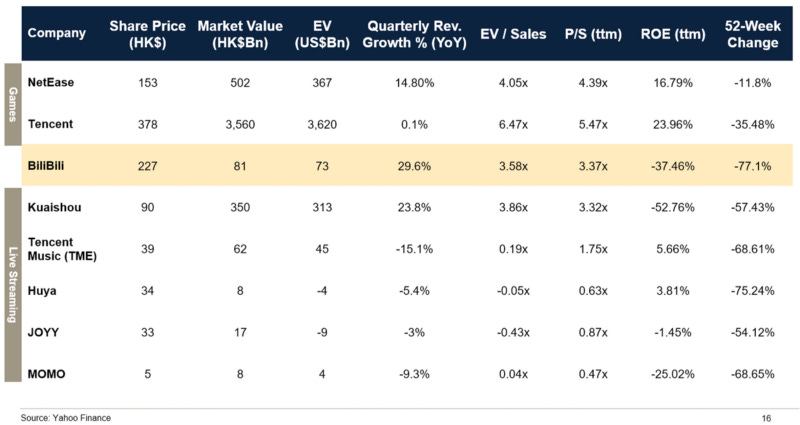

As for comparable companies, BiliBili is fairly valued against their similar-sized peers (i.e., Chinese gaming / video sharing companies) but trade at a discount against industry leaders such as Tencent and NetEase which suggests that they are not as cheap as people thought it would be, despite drawing down c.85% from peak.

Thesis Invalidators — Key Risk

There is a lot of risk for a short in BiliBili and this section aims to provide a summary of them, as well as a structured view of which KPIs you could track post-investment to measure the health of the position. The key risks are:

Loosening regualtory controls on online entertainment — The core of our short thesis is highly dependent on the regulatory headwinds attempting to curb gaming addiction and abolish chaotic fan culture to meet their educational and social goals.

Ability to expand service and establish moat in a highly competitive ACG environment — As previously discussed, we believe that BiliBili will not sustain a highly competitive environment out of their non-ACG user base given the closed ecosystem (i.e., Tightly connected with daily consumption) of tech giants (i.e., Alibaba / Tencent) / mid-cap incumbents (i.e., NetEase / Kuaishou), reinforcing their network effects.

Supply chain recovery sooner than expected — Supply chain disruption plays a huge part in materially damaging BiliBili’s advertisement and e-commerce revenues which is expected to recover at least around 1Q ’23–2Q ‘23.

Higher FDI Inflow to China — Having witnessed significant markdown of Chinese stock within the last 12 months, Chinese stocks may appeal to foreign investors as it trades at cheaper valuation compared to other stocks. An uplift of the system will also affect BiliBili’s price upwards.

Successful cost cutting — This is important to note as BiliBili’ is a loss-making company. Hence, even a slight positive indication to break-even can heavily damage our s hort even if the cost cuts are unsustainable over a long period.

BiliBili launching a successful Flagship Game — As seen with Sea Ltd, one successful game can define a company (i.e., Free Fire). From BiliBili’s track record, they have not been successful at producing games and are buying gaming house to no avail. However, they are one flagship game away from denying us our short.

M&A Risk — As Tencent now considers BiliBili more of a threat than a partner, M&A might make sense if they want to expand their touchpoints / keep exposure to their Gen Z+ community.

However, the first 3 risks mention will hurt us more than being wrong on the bottom-line given the high % of Bili’s shareholders who are fund managers and are more concerned about growth.