Short Summary on Rage Trade

Short Summary on Rage Trade

Rage Trade is an on-chain decentralized Ethereum perpetual swap using Uniswap v3’s vAMM design. The project is built on top of Arbitrum with the main purpose of resolving the fragmentation of liquidity in Ethereum perpetuals through bridging ETH + USD LP tokens from any LayerZero-compatible chains to be deposited into Rage’s 80–20 vault which acts as the liquidity provider for trading on rage.

In actuality, Rage keeps all the deposited LP tokens in the external protocol and uses up to 20% of the value to fully back the deployed capital on rage, keeping the other c.80% as excess margin. This way, the depositor can earn yield from Rage’s trading fees on top of the ones earned from the external protocol. Rage uniquely does not earn any profit / loss from traders as arbitrageurs take away any directional position away from vAMM LPs, providing Rage extra trading fees.

Finally, Rage calculates their funding rate using the TWAP of perp and spot prices. However, if it diverges from CEX funding rates, the protocol utilizes a Chainlink oracle that feeds rates from Binance and updates the rate or manual updates in the worst-case.

Industry Overview / Landscape

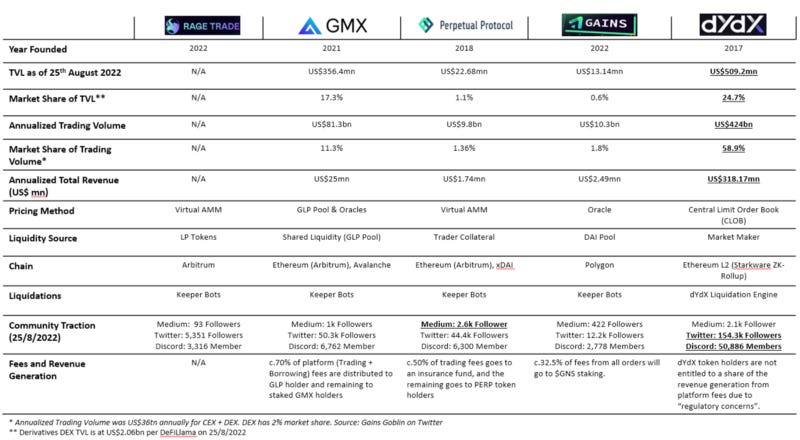

Rage Trade directly competes with other decentralized perpetual markets that offer ETH perps such as GMX, dYdX. Major comparisons between them can be seen below.

dYdX is currently Rage’s biggest competitor processing US$424bn annually, representing c.58.9% of the total derivative market’s trading volume while also processing ~3.65x more per TVL than GMX, an up and coming competitor. As of today, Rage Trade is still in Testnet so there are no comparable metrics aside from decent community traction.

Investment Highlights

TAM: Despite perpetuals being the main source of liquidity to the digital asset space at US$3tn monthly (i.e., US$36tn annualized), accounting for c.66% of all crypto trading volume, the decentralized derivative market is an underpenetrated segment, only processing c.2% of all future / perpetuals trading volume in contrast to the c.13% for decentralized spot market. Furthermore, Perpetuals also witnessed the largest growth of derivatives, growing by an estimated c.358% in comparison to derivative trading volume. This is a huge and sizable market where players such as dYdX, GMX, Perpetual Protocol, and Rage Trade could collectively benefit from a convergence in DEX share of total perpetual volumes.

Business Quality: The protocol generates revenues by charging a c.10% fee on yield generated from vault (i.e., 10%*0.1%*total rage trading volume) and c.0.05% of position size on each trade. This means that c.40% of the total trading fees goes back to the protocol, and the remaining c.60% goes to LP, a 20% premium which is a fair economic distribution given the LPs having to bear the risk of impermanent loss. This will stabilize Rage Trade to be a huge cash generating business. Furthermore, composability through stargate allows them to have better operating leverage than peers when they started as cross-chain deposits are made possible. Finally, unlike GMX, Rage doesn’t act as counterparty to traders which derisks them of highly profitable traders impacting their top-line.

Competitive Positioning: Rage uniquely allows LPs in other protocols to earn extra APY (0.1% of position size per trades in Rage) on c.20% of their LP tokens without having to borrow against it, and no liquidation risk. This capital efficiency is revolutionary in seeding the hard-side of the network (i.e., The LPs). This would then attract traders who are sensitive to high slippages while allowing them to trade with unrealized PnL. This flywheel loop will allow Rage to gain incremental market share from incumbents as the market grows.

Investment Risk

Competition: Rage faces competition from both CEX and DEX. Perpetuals are currently dominated by Binance and dYdX dominates the decentralized perpetual markets. Being a latecomer is disadvantageous with higher customer acquisition costs; traders might already have a pre-existing workflow built on top of the current solutions which is an inertia to adoption.

Low Entry Barrier: Rage’s major value proposition of omnichain liquidity is a characteristic enabled by LayerZero. Therefore, there are is nothing special in terms of technology, and is susceptible therefore we have to over index on their ability to bootstrap and sustain their network of LPs and traders through incentives.

High Demand Fluctuation: Visibility into medium / long-term top-line is minimal as they are very dependent on the highly unpredictable total derivatives trading volume. These protocols are therefore not defensible to external factors, which would highly reflect their multiples.