Post-mortem: Three Arrows Capital

Post-mortem: Three Arrows Capital

The 100,000,000th example of why leverage is bad

Three Arrows Capital or (“3AC”) is a Singaporean-based crypto hedge fund founded by Su Zhu and Kyle Davies in 2012 and had recently planned to move it headquarter to Dubai amidst increasing regulatory clarity in the area. Their last disclosure suggests a peak AUM of US$18bn and now they are on the brink of extinction.

Terra’s Aftermath → 3AC’s Collapse: The Prequel

3AC was one of the victims of Terra/UST’s multi-billion dollar collapse last month, as their initial US$559.6mn/10.9mn position on $LUNC (i.e., was $LUNA before the collapse) position bought in an OTC deal from the Luna Foundation Guard (LFG) back in Feb ’22 is now only worth US$670. There street is speculating that they are trying to recoup their losses through increased leverage in their trading, which backfired and resulted to the US$400mn+ liquidations to date [21].

This catastrophy originated by huge markdowns in $BTC price to which Terra’s downfall was one of the contributing factors (i.e., Terra off-loading massive $BTC supply to support $UST peg). This rippled throughout the market, heavily affecting altcoins from big caps to small caps.

Pre-Requisite: What is stETH?

$stETH is “Staked ETH / Staked Ethereum” for short. It is a derivative product representing $ETH being locked-up on Ethereum’s new blockchain — The beacon chain. One stETH can be used to trade but not redeem 1:1 with $ETH in the market, until Terra happened.

Timeline of the fall

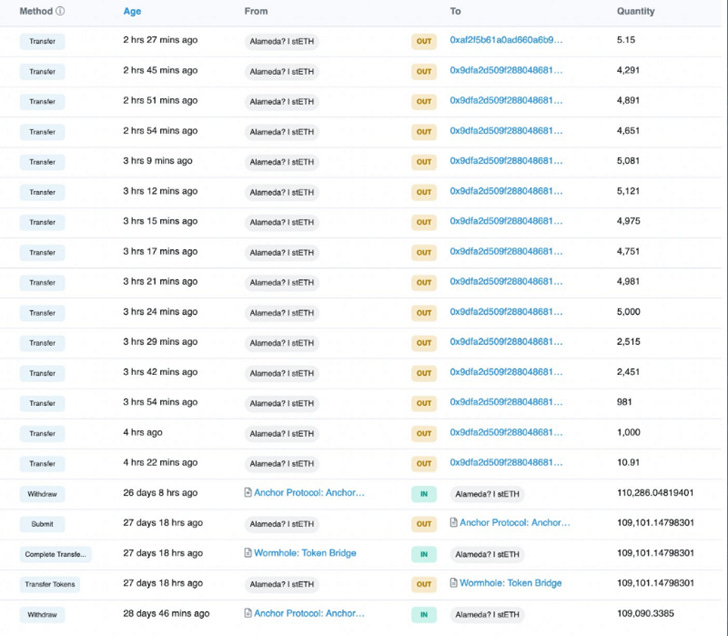

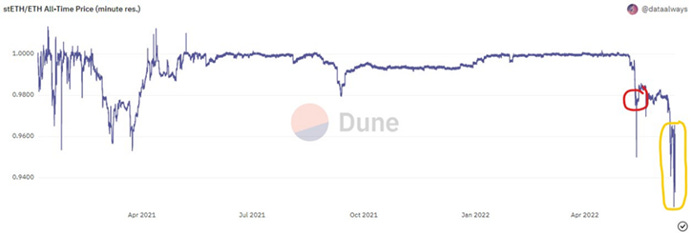

During the Terra / $LUNA fiasco, the stETH / ETH pair “de-pegged” briefly to 0.94 and regained ground around ~0.98 before crashing further on 9th June 2022 when Alameda Research dumped 50,000 $stETH for $ETH as seen below:

3AC was also slowly unwinding their 127k stETH positions from the liquidity pool in Curve worth US$246mn at the time, and US$139mn as of this writing. They went in and out of AAVE and started dumping their stETH for ETH on 14 June 2022. The red circle below co-incides with the time 3AC started withdrawing, and the yellow circle was when they started dumping.

This whole occurrence was bought to light when Moon [7] (i.e., A Twitter User) posted a tweet on 14 June noting that the biggest dumper of stETH was 3AC and not Celsius — the centralized lender who flooded headlines with liquidation concerns due to their over-leveraged stETH positions.

The next morning (i.e., 15 June, 9:00 a.m.), Zhu Su posted a tweet confirming the dire situation at 3AC as seen below:

This sparked savvy twitter-native users to uncover what is currently happening at the firm and went full detective mode — tracking their wallets, analysing transactions to which they found a wallet on Nansen with a 3AC tag although Nansen later clarified that tag was a UI bug but did not dismiss the fact that it does not belong to 3AC.

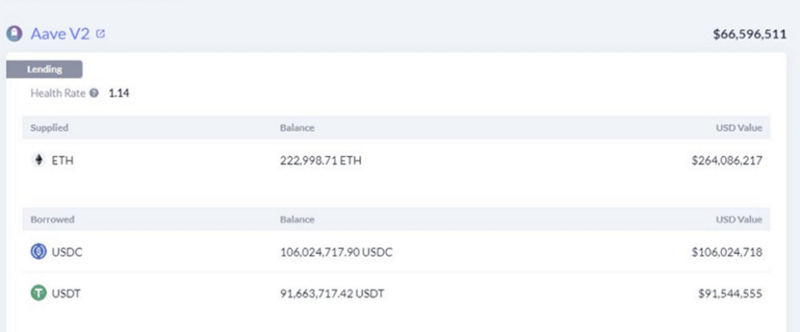

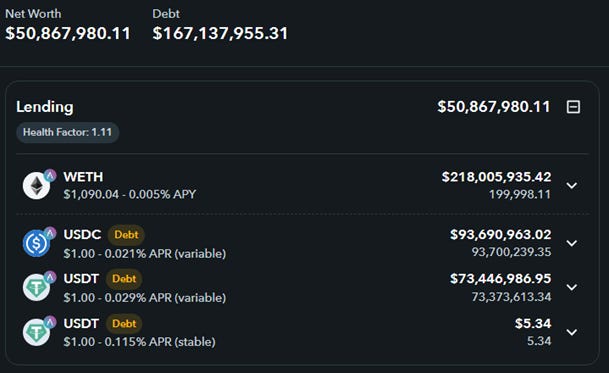

The wallet was found to have pledged a total of 222,998 $ETH as collateral to borrow US$197mn of USDC and USDT from AAVE under the condition that their Loan-To-Value (LTV) ratio is kept below c.85% (i.e., The collateral value shouldn’t drop below 197mn/0.85 = ~US$232mn) which implies a liquidation price of US$1,040 / ETH.

Through scrolling Twitter, and tracking down their other wallet addresses [17], here are several facts & activities to note:

3AC had US$31.4mn realized losses on BitFinex

3AC Withdrew 81,000 $stETH from AAVE (i.e., worth US$92mn during withdrawal) and traded 38,900 of them for 36,718 $ETH via 0x (i.e., A decentralized exchange) on 14/06/2022, representing a c.6% loss on what should have been a 1:1 trade (i.e., stETH / ETH de-pegging).

3AC sent US$90mn of FTT to KuCoin on 15/06/2022, 10:27 am — probably because they don’t want to be tracked and there’s a possibility that they have found an OTC buyer and are sending them through KuCoin so they can’t get tracked. [16]

15,743 $ETH liquidated on compound on 15/06/2022 between 4:07 pm to 5:14 pm [10, 17–20]

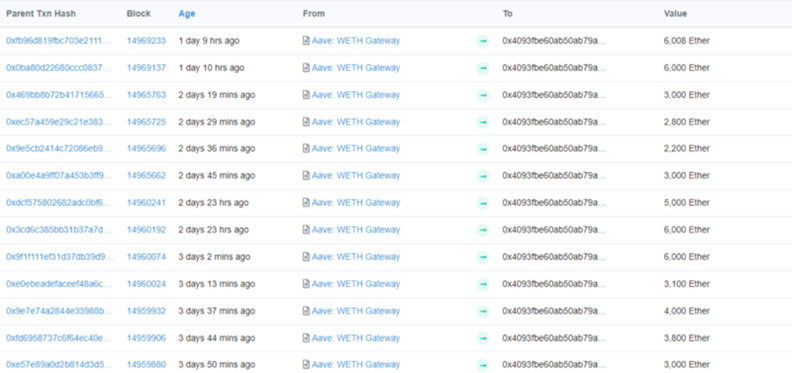

3AC Withdrew a total of 53,908 $ETH collateral from AAVE, sold them for stables, and repaid their loan. [9]

And some rumours to be wary of as well:

3AC liquidated by top-tier exchange, rumoured to be either FTX or Bitfinex

3AC couldn’t meet a US$5mn margin call on a US$1bn loan

As of this writing, this is the wallet’s position:

Analysis: 3AC’s downfall and the impact on the broader market

3AC had US$18bn AUM at peak to which US$9bn is allegedly their VC portfolio (i.e., Invested in BlockFi, Starkware, etc.) marked-to-market, implying the other US$9bn to be their liquid investment. Assuming that the liquid part was 100% invested in $BTC, that portfolio would have drawn down to US$2.7bn (i.e., $BTC is down c.70% from peak).

However, since they were highly exposed to high-risk altcoins as shown below:

It is safe to assume that they would probably be in the sub-US$1bn range prior to the downfall given that their US$500mn+ position on $LUNC (i.e., was $LUNA before the crash) is reduced to ashes and other altcoins are down c.80%-90% from peak. Furthermore, there were even rumours of 3AC pledging their Starkware equity as collateral to respond to margin calls.

3AC is one of the biggest borrower / clients for lenders globally (i.e., Celsius, BlockFi, Amber Group, NEXO, Genesis, etc.) and their collapse would mean a transfer of risk to these lenders who would then have to bear the PnL difference between how much they are owed and what they can get in liquidating the collateral 3AC posted for the loan.

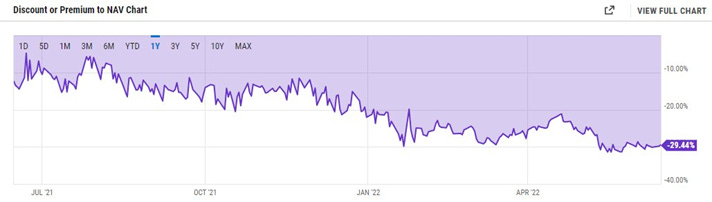

One possible collateral that 3AC could have posted as collateral aside from liquid tokens is their GBTC stake as seen in Figure 9 below. However, the main problem with this is the fact that equities are usually custodied with a 3P Custodian and the process of selling and clearing is not immediate (i.e., Depending on the broker / custodian).

Furthermore, there has been no demand for GBTC at all as seen in Figure 9 below as it is currently trading at a c.30% discount to NAV and dumping c.5% of the total outstanding shares to the market could press the discount further to c.50%.

Hence, this means that if 3AC is going under, there is going to be a minimum of US$100mn in repercussions for lenders even if everything plays out well.

Degen Trading [5] on Twitter suggested there are US$50bn loan creations from aggregate lenders in total and expect a US$30–40 bn wipe out which would draw down the price / liquidity of the cryptocurrency market further. This would widen the bid-ask spread and require funds to post more risk exposure to maintain the same amount of Value at Risk (VaR).

However, the main problem would be increasing pessimism from web3 LPs & other investors in the market. I believe we are going to witness catastrophic redemption, which would cause further de-leveraging. The endgame could either be until the clearance of all the leverage in the system or hope that big institutions would step in and pour liquidity to stomach the drop.

Watch out for BlockFi

3AC has previously borrowed from every single major lender — BlockFi, Genesis, Nexo, Celsius. Celsius has gone under, and it remains uncertain that out of the remaining lenders, who are still exposed to 3AC and to what extent.

I’ve had several suspicions against BlockFi and here are bits and bytes I’ve collected:

BlockFi slashing c.20% of their workforce amidst the 3AC crisis [22]

BlockFi committed to raising another round at a significantly lower valuation compared to previous rounds (i.e., from US$5bn to US$1bn) implying a liquidity crunch, and high possibility of a bank-run.

BlockFi charged US$943k in fines for failing to register securities under Iowa law — not too relevant for the context but worth a mention. [13]

Mixed tweets suggesting problems with BlockFi cancelling withdrawal while there’s no problem with NEXO though this was later clarified by the BlockFi team to which they attribute the issue to the outdated version of the app.

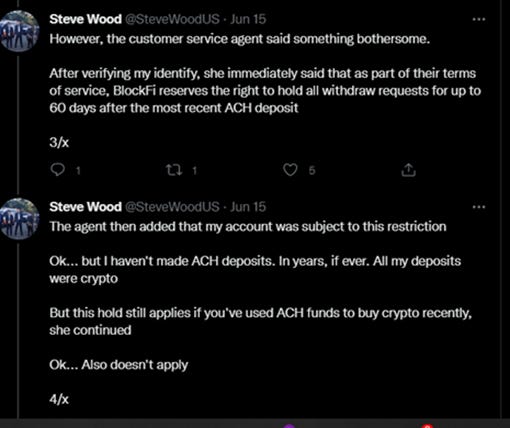

The fact that BlockFi is holding all withdrawal requests for up to 60 days after the most recent ACH deposit (see Figure 12) is also an argument to be made on potential red flags.

Furthermore, Degen Trading [5] claimed that BlockFi had a relatively poor performance compared to their peers despite a bull market, pointing to BlockFi underwriting significant bad debts as a possible explanation which is quite in-line with the SEC’s statement claiming that BlockFi only had c.16% — 24% of their loans being over-collateralized between ’19 and ’21 [14]. The fact that most of BlockFi’s loans are 12-month tenures matches the timeline to which these bad debts might have been incurred (i.e., Disbursement during ’21 bull market).

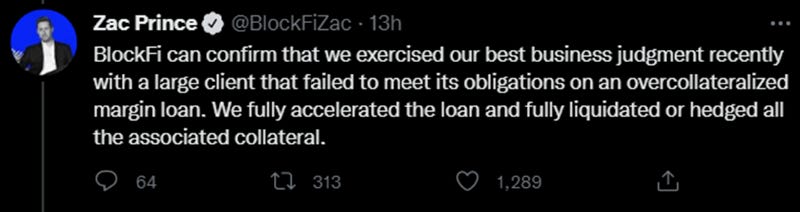

Then, while they were quick to follow up on transparency demands from users after Celsius’ blow up on 13 June, Zac (i.e., BlockFi’s CEO) did not issue a statement for 3 days from the start of 3AC’s liquidity issues till they announced the liquidation of a large client on 17 June which is most likely 3AC:

Assuming that BlockFi operates a US$10bn / US$20bn book, they would have a c.5% — 10% equity buffer as implied from BlockFi’s US$1bn funding [11]. Therefore, a small / mid-sized default from 3AC would mean a significant equity erosion.

No one is safe

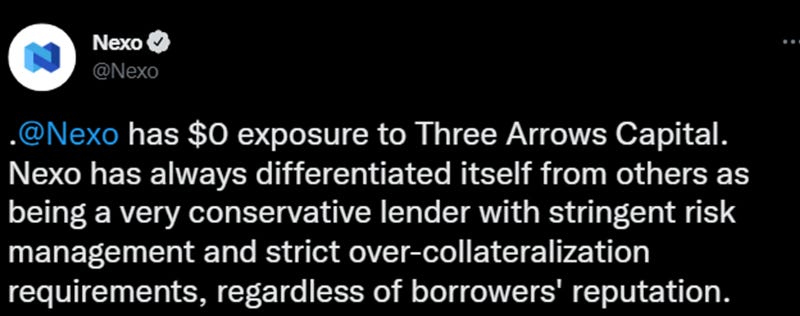

Despite having launched an OTC NFT-backed lending desk with 3AC as their first client back in December ’21 [27], NEXO claims that the business did not take off and they have no exposure to 3AC while also mentioning they did reject 3AC’s request for an unsecured credit back in 2020 [28].

Matrixport, a Singapore-based digital asset platform has issued a statement on LinkedIn that the ‘rapid pace of sell down had resulted in outstanding debt from defaulted loans’ which they claim to have no impact on their solvency after underwriting them.

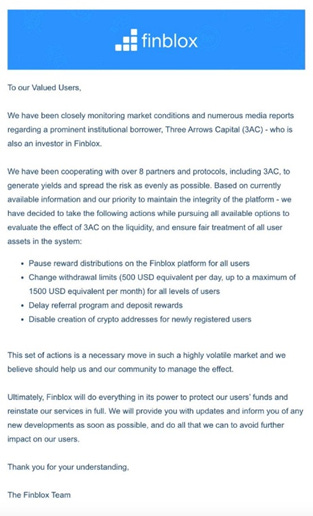

Finblox, a Hong Kong-based digital asset platform has imposed a US$1,500 monthly withdrawal limit due to their exposure to 3AC.

Thoughts:

Stringent risk management practices might sound nerdish /off-setting in a bull market but is the only thing that will keep you going through a bear market.

Competition is healthy until PED is used.

Watch out for the next token unlocks of 3AC’s primary holding (See Figure 8) as they are most likely dumping them to meet margin calls / as part of asset liquidation during bankruptcy.

and Finally:

Trouble brewing: Three Arrows Capital ghosting 8 Blocks Capital

8 Blocks Capital (8BC) is a delta neutral market maker in crypto base in Hong Kong. They entered into an agreement with 3AC back in 2018 where 8BC would pay 3AC a fee to use their trading accounts.

Since 8BC is very sensitive to trading fees, the agreement was structured so that 8BC can withdraw whenever they want and 100% of PnL belongs to 8BC and 3AC Is never to move funds w/o permission and 8BC will pay 3AC for service.

When the market tanked on June 12, 2022, 8BC needed some funds to cover other positions on other exchanges and asked for withdrawal to which was successful. However, the subsequent withdrawal which 8BC requested on 13th June 2022 was ignored but since 8BC don’t need the second withdrawal as market calmed, they did not instigate further.

On June 15, 2022, 8BC noticed that ~US$1mn was missing from their account through their fund monitoring script and they reached out to Kyle Davies (i.e., 3AC’s co-founder), and the operations team on Telegram to which there were no replies.

8BC soon finds out that 3AC were leveraged long in many platforms and were getting margin called as the market tanks. However, instead of answering the margin calls, they ghosted everyone, and platforms had no choice but to liquidate their positions which further dumps the market.

Reference

§ [1] Times Tabloid — 3AC’s LUNA position worth $670 from ~US$500bn+

§ [2] Etherscan — 3AC pulled out 127,762 stETH from Curve

§ [3] Twiiter — Defiyst 3AC thread

§ [4] Twitter — Danny Yuen’s 8BC/3AC Thread

§ [5] Twitter — hodlKRYPTONITE 3AC Thread

§ [6] Zapper — 3AC AAVE wallet

§ [7] Twitter — MoonOverlord Thread on 3AC dumping stETH

§ [8] Twitter — MidasTheFool 3AC Thread

§ [9] Etherscan — 3AC AAVE Wallet

§ [10] Etherscan — 3AC Compound liquidated tx

§ [11] Crunchbase — BlockFi

§ [12] The Block — BlockFi raising at lower round

§ [13] Iowa Gov — BlockFi Fined US$1mn

§ [14] Schneider Wallace — BlockFi Un-Collateralized loans

§ [15] BlockFi — Prime

§ [16] Etherscan — 3AC sent US$90mn of FTT on KuCoin instead of FTX.

§ [17] Dune Analytics — 3AC Wallets

§ [18] Twitter — 3,346 ETH liquidation on Compound

§ [19] Twitter — 1,716 ETH liquidation on Compound

§ [20] Twitter — 2,681 ETH liquidation on Compound

§ [21] Blockworks — Crypto Fund Three Arrows Capital Facing Insolvency

§ [22] Fast Company — Crypto layoffs as token crash

§ [23] Business Times — BlockFi decides to raise at a lower valuation

§ [24] BlockFi — Withdrawal Rules

§ [25] Twitter — BlockFi liquidates large client

§ [26] Twitter — Why the lenders are in trouble and why you should be worried.

§ [27] Coin Telegraph — Nexo price drops 40 in three days on rumours

§ [28] Twitter — Nexo claiming 0 exposure to 3AC

§ [29] CoinDesk — Finblox imposes monthly withdrawal limit amid 3AC uncertainty