Market Study: Investing in DevOps

Market Study: Investing in DevOps

A Thematic Guide

Executive Summary

Ideated in 2007, DevOps is best described as a set of 1) practices, 2) tool, and 3) cultural philosophy that automate and integrate the process between software development and other IT teams (operations, security, etc.), allowing organization to deliver applications and services at higher quality and velocity. The key idea centres around merging the Development and Operation team to collaborate across the entire software development lifecycle (SDLC).

The DevOps software market has gained significant traction over the past decade, topping a US$6.6bn industry in 2022 and is poised to grow at a c.21.5% CAGR to US$25.8bn by 2028. The proliferation of DevOps adoption is headed by 3 structural macro tailwinds:

Increased adoption of Cloud and SaaS based delivery

Highly competitive software market stemming from lower entry barriers necessitates higher internal efficiency to remain competitive

Shift of purchasing power towards developer and proliferation of AI eliminates significant cultural & technical barriers towards DevOps adoption

Increased Adoption of Cloud and SaaS-based delivery

The premise of cloud is to shift one’s entire computing infrastructure to a centralized server online, which is called the ‘cloud’. By hosting software, platforms, and database remotely, companies significantly reduce overhead required to scale infrastructure. These services usually charge customers on a usage basis. Hence, it is also coined as Software as a Service (SaaS). This technology started in 2006 when Google’s CEO Eric Schmidt introduced the concept at an industry conference.

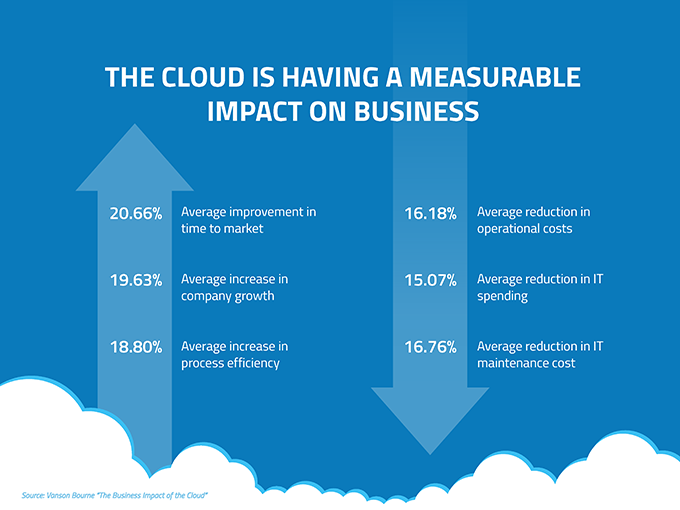

Cloud has seen unprecedented adoption with — 1) c.50% of enterprises spending more than US$1.2mn annually on cloud solutions, 2) c.79% of workloads currently exist on public and private clouds. End-user spending on cloud services is poised to grow at a c.10.1% CAGR, topping US$727bn by 2025.

The shift towards cloud was a major step towards democratizing infrastructure scaling. This represents one of the most fundamental changes to the way software is build, sold, and integrated since the migration of models from mainframe to client / servers.

This initiates the development of cloud-native tools, APIs, and Infrastructure as Code, which reduces significant friction for rapid software development, provisioning, networking, and deployment, accelerating the Software Development Life Cycle (SDLC). This dynamic shift induced notable changes from the demand-side (i.e., Software clients), requiring purchased software to — 1) Be available 24/7 without downtime, 2) Enable dynamic user scaling, 3) Support complex infrastructures, and 4) Handle frequent updates to adapt to ever-changing end-user requirements.

Cloud adoption has also accelerated the adoption of the microservices architecture. Previously, software applications are built on top of a single code base from a single platform. However, as software gets increasingly complex, % of software sourced from a dependency (i.e., Reusable package, Library, Module, or artifact) has increased from c.15% in 2000 to c.85% in 2021.

This led to an increasing need for code reusability and modularity / the microservice architecture — breaking down an application to smaller, decoupled components which are independently deployable and are usually owned by small teams. Therefore, tools that enable de-coupling of components were increasingly sought after. For instance, Docker pioneered the rise of application containers, which enabled the de-coupling of application runtime and host OS on the virtual machine. The application container market has grown to a US$4.3bn ARR at a 5-year c.30.8% CAGR and is expected to grow at a c.26.8% CAGR, reaching US$17.9bn by 2028.

This new approach towards creating and maintaining application creates new requirements and complexities for cross-functional developers and operations teams which accelerated the need to embrace DevOps practices and tooling towards increasing collaboration efficiency.

Increasingly Competitive Software Market

The software market has matured tremendously compared to decades ago with the market at US$672bn in 2020 vs US$244 bn in 2010 vs US$100bn in 2000 (see below). The democratization of low-cost software infrastructure (i.e., Through cloud) has lowered the barrier of entry, which led to high competition amongst category leaders and emerging players gaining market share. Hence, organization will have to place higher emphasis to optimize for efficiency more than ever.

DevOps is well credited to have optimized the SDLC through 2 angles — 1) Lower cost, and 2) Higher speed. DevOps optimizes for cost through the following way:

Automating CI/CD process and provisioning of IT infrastructure: The proliferation of IaC (i.e., Infrastructure as Code) which allows the automation and re-use of template-based solutions to provision infrastructure has significantly lowered cost and accelerated development time as compared to manual provisioning.

Leveraging 3P services: DevOps embraces plugging in 3P services and only create an IT infrastructure / service from scratch whenever customization is needed (i.e., Read Netflix’s Case Study below). This prevents teams from spending unnecessary time and money, significantly reducing operational overhead.

Others: DevOps also optimizes cost through — 1) Incentivizing good application design, 2) Reducing switching costs, 3) Reducing employee turnovers, 4) Minimized downtime as recovery is often expensive. Furthermore, as DevOps iteratively tests throughout the SDLC, they capture errors in the early innings of the workflow, preventing errors to accumulate as costs to fix at the more mature phase gets exponentially expensive (see below).

Asides from cost optimization, there is a high correlation between adopting DevOps towards faster development lifecycle. This is crucial as development velocity is linked towards faster product innovation, allowing companies to enjoy significant benefits such as first-mover advantage, and reduced churn, etc.

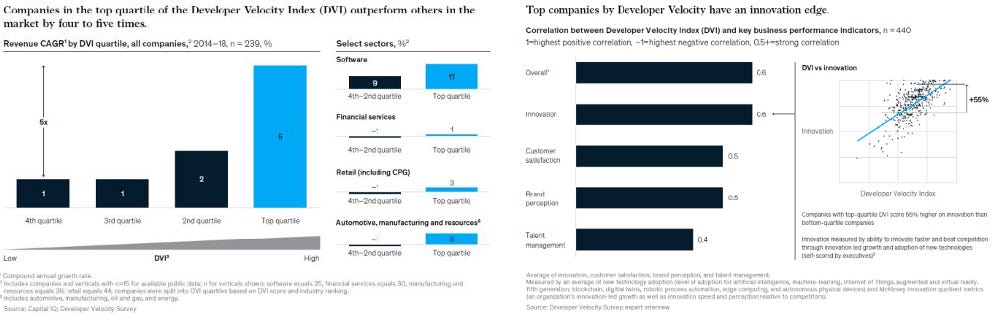

Through analysing the technologies, working practices, and enablement of various organizations, McKinsey has developed an index called the Developer Velocity Index (DVI). The index highlights the importance of developer velocity as — 1) Top-quartile DVI scores are correlated to 4–5x higher top-line growth vs bottom-quartile companies, 2) Top-quartile DVI companies exhibit c.60% higher ROIC and c.20% higher EBIT margins vs bottom-quartile companies.

Furthermore, companies with top-quartile DVI scores shows c.55% higher on innovation than bottom-quartile companies. This suggests that focusing on improving developer velocity which has been the main premise of DevOps is huge towards building / improving one’s competitive advantage. This is especially crucial in a market with fast-changing end-user requirements.

Shift of Purchasing Power towards Developer

Despite the significant benefits of adopting DevOps, only c.40% of the applications today are DevOps-enabled while scaling remains a challenge (i.e., less than 30% of organizations are classified employs highly evolved DevOps practices).

Through studies from various DevOps reports, the deal team concludes that — 1) Cultural, and 2) Technical blockers are 2 categories of barriers impeding massive DevOps adoption with the latter more prominent in lower evolved DevOps organizations. However, we are witnessing trends in the industry that suggests structural alleviation of these frictions.

Cultural Blocker: Through a study conducted by Bain & Company in 2021, they have observed that c.36% of respondents rank cultural resistance being the top-3 challenges to scale DevOps. Furthermore, studies conducted by Puppet, Google, and Dynatrace also reported similar results — adoption and scaling DevOps enterprise-wide is often not well-received.

A trend that is observed in the industry is the shift of the buying centre from a top-down approach to a land-and-expand, high velocity GTM approach targeting practitioners (i.e., Developers). This means that the initial entry point will be a single cheap offering to be purchased by a development team member (“Land”) where word of mouth and additional product offering will drive upsell within the organization (“Expand”)

This approach has been proven to achieve better sales efficiency compared to the traditional top-down approach as when researching new tools, most developers rely either on — 1) Free trail (c.77% of respondents) or 2) Word of mouth (c.68% of respondents).

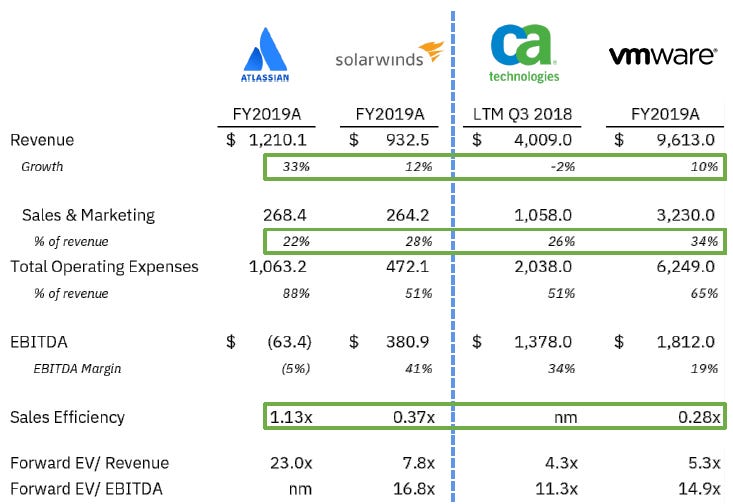

As seen below, Atlassian / SolarWinds’ low-touch, word-of-mouth driven approach has allowed them to experience higher growth rates compared to legacy vendors with enterprise-selling models such as CA / VMWare.

The shift of decision-making away from C-suite to practitioners (i.e., Developer) is a major step towards mitigating the cultural barrier as developers are focal towards the pain points within the SDLC workflow. Furthermore, demands will be more efficient as they stem directly from the practitioners.

Technical blocker: Through a study conducted by Puppet / Dynatrace / Google on the State of DevOps in 2021, the deal team has witnessed Technical Complexity as a significant barrier towards mass adoption (see below — left) which translates to lack of sufficient skills amongst employees from another viewpoint (Per Atlassian’s DevOps survey).

This has led to huge trade-offs between maintaining quality and accelerating delivery. To address this issue, the deal team has witnessed an c.34% CAGR growth in AI spending on application development (i.e., Code, delivery, and remediation across SDLC). This is expected to lower barrier of adoption through automating complexities, especially among SME where DevOps adoption rate is lowest due to steep learning curves.

Benefits of implementing DevOps

Through embracing key DevOps practices, tools, and organizational philosophy, companies can differentiate themselves through — 1) Accelerated time to market through faster development cycles, 2) Increased adaptability towards market conditions through faster feedback loop, 3) Improve reliability and quality of application during updates through automation and consistency, 4) Faster and more effective post-mortem recovery while improving team collaboration at scale.

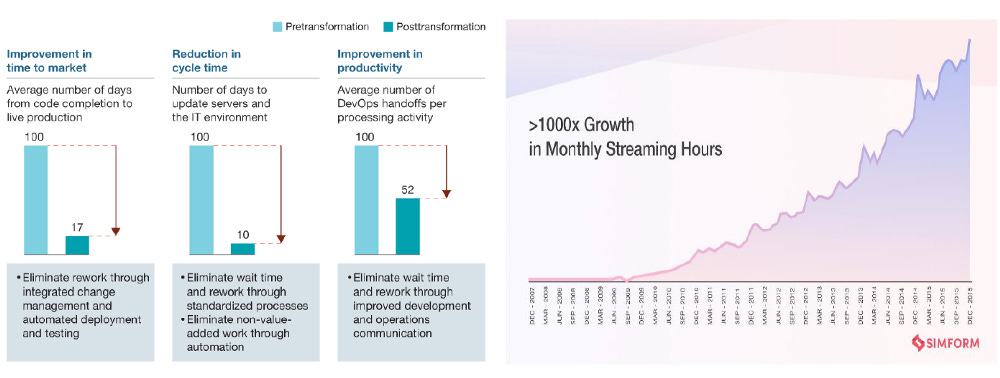

For instance, implementing DevOps has seen an accelerated development (coding) and SDLC by a factor of 30 and 8,000 respectively. Another example of value capture would be how Netflix’s emphasis on improving developer innovation velocity has enabled them to deliver fast features to customers, scaling their business 1000x in terms of monthly streaming hours in the first 7 years of their shift (see below).

Investment Thesis

In the past decade, DevOps have been gaining traction as a transformative Software Development methodology capturing value for the overall businesses (as discussed previously) while benefitting the stakeholders in the SDLC with increased efficiency, accelerating problem solving, increased feedback / responsiveness, ultimately improving satisfaction.

With increasing demands for business agility and shifting consumer demands for faster software innovation, affecting all major industries — Dynatrace expects that c.40% of the software in 2023 will be DevOps-enabled form c.10% in 2017.

The emergence of Cloud / SaaS-based software delivery, significant shift towards a more modular approach in software development — microservices, and integrated security had been the forefront drivers for significant DevOps adoption.

However, the market for DevOps tooling / enablement is still relatively early in the broader software landscape — this is simply because from the ‘State of DevOps’ reported by either Google / Puppet, the % of correspondents fitting the high DevOps evolution bucket is still low at < 30%. Bain also reported in their 2021 DevOps report that only c.12% of their respondents describe their DevOps capabilities as mature.

Therefore, the core thesis beyond the proliferation of DevOps is 2-fold:

Increasing DevOps penetration beyond c.40%, and

Increasing % of correspondents fitting the High DevOps evolution bucket.

This will require the next wave of DevOps tooling to bridge / alleviate both cultural / technical barriers hindering the adoption and scaling of DevOps (i.e., Lack of standardized tools, Complexities in implementation, etc.)

The Overall DevOps market currently hovers at US$6.6bn and is expected to grow at a c.21.5% CAGR to US$25.8bn by 2028 on the back of — 1) Continued SaaS / Cloud adoption, 2) Increasing adoption of microservice architectures amongst organizations, and 3) The increasing need to innovate product faster at lower cost to keep up with competition.

Furthermore, it is expected that Asia-Pacific will be leading the pack in terms of growth at a c.26.4% CAGR on the back of — 1) Extensive digitization across sectors (esp. in IT & Telcos), and 2) Rapid adoption of automated software delivery tools to streamline operations amongst SME to reduce Capex by integrating hybrid cloud solutions with CI/CD tools.

However, despite the growing array of DevOps tooling, the deal team believes that only a fraction will see the light of mass adoption and is heavily reliant on how well the tool reduces cognitive overload related to any non-core developer workflows. The rationale behind this is because humans are not capable to adapt to ever-increasing proliferation of technology given the massive difference of the rate of progression between the two.

Therefore, the most sensible way forwards are so that tools should be designed in such a way that developers (i.e., Humans) will not need to keep up with new technicalities and focus on what they do best. These tools can be identified based on features that simplify the Developer’s workflow / experience / journey. Examples of such features are:

Tools that heavily automates manual / redundant / non-core processes

Tools that abstract away non-developer workflows (i.e., IDP automates provisioning which is done by the operations team)

End-to-end capability suite (i.e., Tools that cover all testing capabilities > Tools that cover only some). This encourages consolidation within a specific value chain.

Tools that organize services crucial to Developer’s workflows (i.e., Service catalogues)

Tools with lower learning curves

Tools that incorporate the developer’s pre-existing fundamental knowledge (i.e., Git workflows)

Here are 6 identified categories to be at forefront of the next wave of DevOps tooling:

Investment Thesis #1: End-to-End Testing Automation

Despite the recent emergence of test automation, testing remains a significant bottleneck towards a faster delivery cycle as c.80% of testing is still manual — US$22bn is spent annually on QA/Test services which is 10x greater than the automated testing tools market.

The current automation tools mostly cover Unit / Integration testing, with end-to-end testing (i.e., Validating whether application meets the system requirements) remaining mostly manual. To combat this, teams have tried customizing their test automation frameworks, which often backfires as it is — 1) Time consuming to onboard new team members due to steep learning curve related, 2) Maintenance of these tools being costly.

Through numerous attempts, there’s an industry-wide understanding that the major challenge with these testing solutions is the high coding skills / expertise required to create and maintain scripts. Therefore, “loss of expertise” has been the major cause of churn at many automation vendors.

Therefore, there is a two-fold value capture in the rapidly expanding US$2.7bn Test Management and Automation market — 1) Democratizing automation testing, and 2) Leverage AI/ML to develop end-to-end testing capabilities, reducing the test lifecycle and hence, faster software release.

Furthermore, the fragmentation of the current automated testing market provides a ‘white-space’ for players to consolidate solutions given high degree of overlapping offerings amongst players.

Some of these end-to-end testing companies can be seen below:

Investment Thesis #2: Internal Developer Platform Frameworks

Despite increasing DevOps adoption rate from c.10% in 2018 to c.40%, there are varying degrees of DevOps maturity in an organization which is perfectly capture in the diagram below:

Different reports on the state of DevOps had surfaced, classifying different organizations into different bucket of DevOps evolution. For instance, Google classified them into 4 (Elite, High, Medium, and Low) while Puppet classifies them into 3 (High, Mid, and Low). The main problem lies in the fact that organizations belonging to the top bucket (Elite / High) are minorities (< 30%).

It is crucial that organizations reach the elite / high DevOps bucket respectively given that these groups are — 1) 973x faster in code deployment, 2) 6,570x faster in lead times from commit to deploy, 3) 3x less likely to fail from changes, and 4) 6,570x faster mean time to recovery.

Organizations usually face significant challenges in scaling DevOps enterprise wide as Dynatrace cited that there are lack of consistency for the SDLC workflow given the rapidly expanding toolchain / services used. (i.e., c.71% of respondents say that unified end-to-end platform integrating their toolchain is critical for scaling).

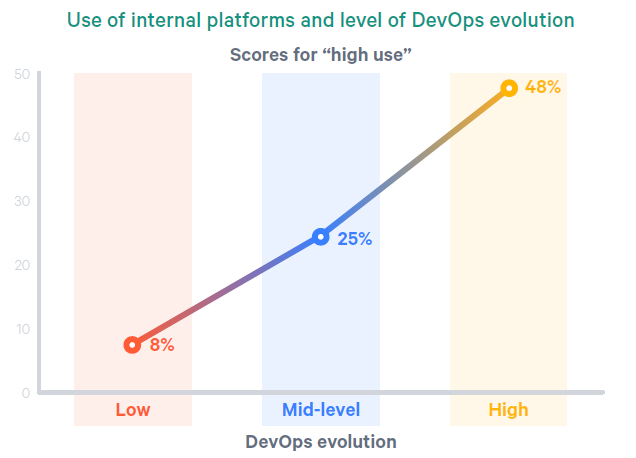

The use of Internal Developer Platform (i.e., A foundation of self-service APIs, tools, services, knowledge, and support arranged as a compelling internal product) has been highly correlated with higher DevOps evolution as shown in the figure below.

Internal Developer Platform (IDP) allows developers to self-serve their provisioning needs — streamlining application configuration and infrastructure management, this frees up operation team from handling repetitive task and eliminate the need for developers to wait for operation teams to provision the infrastructure manually.

However, a common overlooked fact is that the best results on Internal Developer Platform is when application components are also made available via self-service, not only infrastructure components. For instance, organizations in the low-mid evolution groups are 7.5x more likely to have infrastructure components automated / available for self-service (i.e., VM Provisioning) rather than developer components (i.e., Building blocks for observability, rate limiting, source IP geolocation routing).

Therefore, this brings forth the following value creation avenues:

Increasing need for IDP increases market for as-a-service frameworks: These are the frameworks / building blocks to build an IDP. For instance, Humanitec is a lightweight platform API connecting to underlying infrastructure, and Gimlet is a SaaS platform offering a simple infrastructure orchestration, environment, and deployment management platform. The Global Integration Platform as A Service (IPAAS) market is expected to grow at a c.37.2% CAGR to US$23.71bn by 2028.

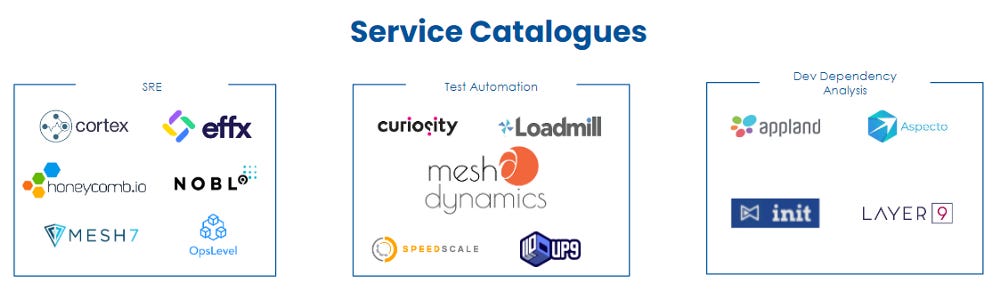

2) Increasing demand for Service Catalogue to complement IDP: Service Catalogue acts as a digital registry which makes services and their metadata easy to understand for enterprises to see, find, invoke, and execute services regardless of where they are in the company. They complement IDP’s workflow as service catalogue’s service doesn’t come with dependencies to database(s), routing, storage, secrets, and everything else that would be needed to deploy a set of services or applications to the infrastructure — Developers can self-serve these through the IDP. This is a market that is still in its early innings with a potential to reach US$1.17bn at a c.10.1% CAGR by 2026 [35]. There are 3 groups of service models which are on the rise as seen below:

Service Models Automating Test Automation: Through understanding relationships between services and end user transactional flow, tests bed can be automatically generated and maintained — enables new change to be introduced faster by reducing the complexity.

Service Models for Site Reliability Engineering: SRE measures service level objectives (SLO) and work on incident resolution require a metadata model that connects transactional behaviour with meta information about the services (i.e., Code, developers, user behaviour, tools to make changes).

Service Models for Development Dependency Analysis: As software scale, small changes can have large impacts upstream and downstream. Service metadata aids developer in planning and implementing changes.

3) Under-addressed market for Internal Development Framework to include self-service of developer component: As previously mentioned, IDP is maximized when both infrastructure and developer components are available via self-service. Therefore, this presents an opportunity for these IDP frameworks to integrate open-source drivers for developer components (i.e., Observability with Datadog, Testing with Postman) with their API.

Investment Thesis #3: Increasing shift of Go-To-Market targeting developers accelerates the adoption of products that improve developer’s experience

The shift of initial point of entry for tooling from C-suite management to the developers themselves has accelerated adoption (i.e., Witnessing larger revenues, more VC, and higher valuation) of products that improve developer’s experience / bridge the “Developer Experience Gap” [33]. The “Developer Experience” tooling includes:

1)IDE / Build Tools: Having additional tools that help with other portions of the SDLC within the IDE allows developers to lower the need of training newcomers as the UI are usually intuitive to those concepts. Notable players in this space

Microsoft VS Code: 108k GitHub stars

JetBrains IntelliJ: Most profitable IDE, parent company reported US$200mn EBITDA

Others: Sublime Text, Emacs, VIM.

2)Git / Command-Line Interface Workflows Embedded in Developer Lifecycle: Through consolidating a command that developers have executed numerous times (Git’s Push / Pull / Deploy / Commit / Terminal Experience) to a workflow leads an improved in development velocity. Notable players in this space:

Heroku: PaaS offering a workflow leveraging git command to a version control repository. They were acquired by Salesforce for US$200mn.

Hashicorp (NASDAQ: HCP): Provides consistent workflows to provision, secure, connect and run infrastructure. They have mastered command line interface flows for infrastructure building blocks.

Netlify: Optimizes deployments for web application — combining hosting infrastructure, CI/CD into a single automated workflow through connecting an existing Git repository. They have ~1mn+ developer accounts.

Vercel: Adds to git flow by providing a staging URL on every commit, better optimized for starting from a Web framework template / headless CMS.

3)Pull request Workflows Integrating Cybersecurity & Compliance into Code Reviews: Pull Request (PR) acts a gatekeeper — preventing changes from advancing to later changes in the delivery cycle. By checking for application security, and compliance, they reduce time, cost & complexity of maintaining downstream integration environments. Notable players in this space:

Snyk: Authentic integration of Software Composition Analysis (SCA) into the PR workflow, creating the impression that developers can execute on application security. They have bagged US$1.4bn in funding, valued at US$8.6bn.

Others: Atomist.

4)ChatOps Platform: Biggest bottlenecks within developer teams are communications between stakeholders (i.e., Discussing specs / PR / Feedback Coordination). ChatOps platform eliminate the manual coordination overhead essential for discussion relating to SDLC (i.e., Issue / PR / Alerts). Notable players are:

Slack: Acquired by Salesforce for US$28bn.

MS Teams: 20mn Weekly active users. Like Slack, they modernize chat by delivering it as a bot platform, group members can interact with each other and with IT system through bots.

Nimbella and CTO.ai: Delivered extension to their DevOps automation and serverless platforms making it simple for teams to create new ChatOps workflows.

Investment Thesis #4: Increasing complexity for SaaS & Cloud Architecture emerges the need for Progressive Delivery (i.e., Consolidation of CI/CD, GitOps, Experimentation)

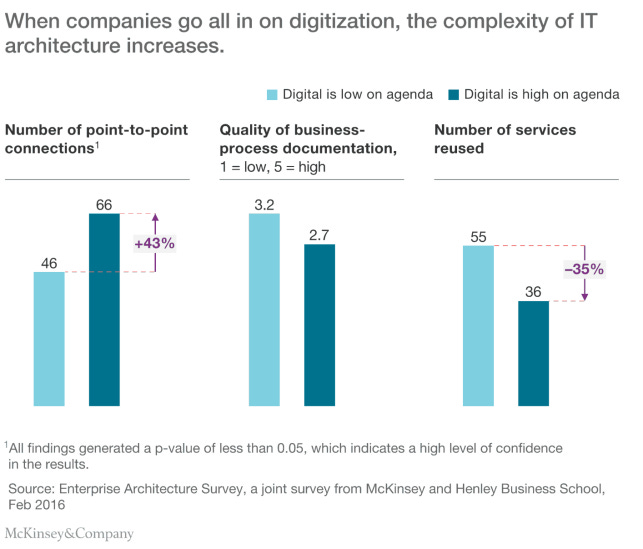

To enable interoperability between applications hosted in the cloud, companies have witnessed magnification of complexity within their IT infrastructure (i.e., Companies with high digital agenda witnessed +43% point-to-point connections).

This drives the need for more dynamic, and adaptable deployment, de-emphasizing a sole focus on configuration management. Instead, focusing on a more pragmatic approach to enable organizations to be more continuous over time.

This approach is coined ‘Progressive delivery’ which incorporates elements of CI/CD, configuration management, GitOps, and experimentation together.

Furthermore, the roadmaps of vendors in each of the segments forementioned are converging with one another (i.e., CI/CD vendors incorporating GitOps / etc). Combined, there are ~30 products generating $500mn ARR growing >20% CAGR to create this mega market.

The consolidation will end up with vendors merging / acquiring capabilities along the value chain. The one who will lead the pack / gain the most market share has to be able to provide the following functionalities easily and more thoroughly:

Developer-adopted feature flags and AB testing

End-user behaviour analysis and experimentation controls for PMs and product teams

Cultural and process transformation services to enable delivery transformations

Continuous deployment, automation, configuration, and assurance engine that reliably moves changes from one environment to another.

Investment Thesis #5: Increasing complexity for SaaS & Cloud Architecture emerges the need for Progressive Delivery (i.e., Consolidation of CI/CD, GitOps, Experimentation)

As companies view software as their ‘competitive advantage’, the need for higher engineering velocity which was highlighted beforehand (i.e., Companies with engineering velocity exhibit 4–5x higher top-line growth, c.60% higher ROIC, c.20% higher EBIT margins, and c.55% higher product innovation) becomes more imminent.

Value stream management ($200mn ARR, c.20% CAGR) is a solution that has existed for quite a while. They provide visualization / visibility to where value is created in a process within the delivery lifecycle. In short, providing visibility over the business’ service level agreement (SLA). However, there VSMs does not provide visibility over the software engineering process (i.e., The process required to achieve the corresponding SLAs / The organization’s technical SLOs).

This introduces a new sub-segment which brings in observability for the software engineering process — Engineering Efficiency (US$100mn ARR, c.35% CAGR). These tools integrate and source metrics from every tool in the software engineering value chain to diagnose and provide optimization suggestions accurately. This is an attractive market to explore given that there is a strong moat to be build around maintaining integrations across an increasing number and complexity of observability points.

Investment Thesis #6: Lack of integration and end-to-end solutions provides an opportunity for aggregators within DevSecOps

The rapid growth of the US$327bn systems integration market (i.e., Driven by the proliferation of Cloud / IoT / Distributed Systems) which places applications, data, and users outside the confines of a data centre’s firewall has seen fragmentation at the application and service level, pointing to a continually expanding threat surface — Every developer / developer tool / developer infrastructure / developer process is a potential entry point for bad actors to compromise code, inject malware, copy IP, or disrupt automation.

For instance, the SolarWinds 2020 hack was done through a code injection in their CI/CD infrastructure despite having a clean code within their version control repository. Therefore, practitioners / CSOs need to acknowledge the broad scope of software security.

This induced the increasing need for a secure supply chain. This means that software security needs to be — 1) Shift-left rather than done after production, and 2) Build-in rather than coming from the outside given the lower cost associated with fixing vulnerabilities earlier and the increasing risk of cyber attacks respectively.

Despite vendors such as Snyk, snyopsys, etc… venturing to this space, there are still 2 main bottlenecks for software security / DevSecOps — 1) How to insert DevSecOps into the practitioner-led adoption motion common with Dev and Test teams, and 2) No vendor has provided a complete suite of offerings.

References

▪ [1] SalesforceDevops — Evolution of DevOps

▪ [2] IBM — DevOps, a complete guide

▪ [3] Atlassian — Test Automation

▪ [4] TechTarget — DevOps Ultimate Guide

▪ [5] Clickittech — DevOps Team

▪ [6] Puppet — 2021 State of DevOps

▪ [7] Amazon — Continuous Integration

▪ [8] Bain & Company — DevOps Tech Report 2021

▪ [9] AppDynamics — NoOps the end of DevOps

▪ [10] Google — 2021 State of DevOps

▪ [11] Statista — SaaS End-User Spending Worldwide from 2015–2023

▪ [12] Statista — Public Cloud Services End-User Spending Worldwide from 2017–2023

▪ [13] Substack — Tyler Jewel on Trends Fortell New Approaches to DevOps in 2021

▪ [14] Statista — IT spending on enterprise software worldwide, from 2009–2023

▪ [15] McKinsey — Developer Velocity: How software excellence fuels business performance.

▪ [16] Capsule8–5 Barriers to DevOps Deployment

▪ [17] IDC — IDC Forecasts Improved Growth for Global AI Market in 2021

▪ [18] McKinsey — Beyond Agile: Reorganizing IT for faster software delivery

▪ [19] Simform — Netflix DevOps Case Study

▪ [20] Visual Paradigm — What is Agile Software

▪ [21] Intellipaat — SysOps vs DevOps What’s the difference

▪ [22] Snyk — What is DevSecOps?

▪ [23] Forrester — DevOps M&A Activity

▪ [24] Shea & Company — DevOps Market Map

▪ [25] Investec — DevOps Market Report

▪ [26] BCG — Navigating Competitive Software Mergers Acquisition Market

▪ [27] Medium — Comparing Publicly Traded DevOps Companies

▪ [28] Codacy — Fragmentation vs Consolidation

▪ [29] Dynatrace — 2021 State of DevOps

▪ [30] Everest Group — Fragmented DevOps Landscape

▪ [31] Chef — What is an Internal Developer Platform?

▪ [32] Medium — Problems in Adopting DevOps

▪ [33] Redmonk — Developer’s Experience Gap

▪ [34] Humanitec — Backstage Service Catalogue

▪ [34] Humanitec — What is an Internal Developer Platform?

▪ [35] Businesswire — Global Catalogue Management Systems Market Size

▪ [36] Sky High Networks — Cloud’s measurable impact

{kind=link}

▪ [37] Medium — Microservice vs Monoliths

▪ [38] MuleSoft — When iPaaS goes awry don’t accelerate your point-to-point connections

▪ [39] Microsoft — SolarWinds 2020 Hack

▪ [40] Medium — Airbnb’s microservice architecture journey to quality engineering

▪ [41] QEunit — MAMOS

▪ [42] Internal Developer Platform — Tools